Fewer bad loans. Better repeat borrowers.

All white-labeled to your brand.

Give your borrowers a real deal analyzer before they submit. They show up with a real ARV, a real repair scope, and real comps. Your team underwrites a cleaner file.

The deals that eat your margin are the ones that never should have been submitted.

Fantasy ARVs. Thin comps. Rehab numbers pulled out of the air. The borrower doesn't know what they don't know, and your team pays for it in hours, risk, and lost repeat business.

Files that never should have been opened

Borrowers submit with ARVs $40K too high and rehab budgets at half of reality. Your team spends 2 to 4 hours per file before rejecting it. One a week is annoying. Five is a headcount problem.

Deals that fund on bad math

The wishful ARV becomes your LTV problem. The missed holding costs become the reason a borrower can't refinance out. You end up owning the outcome of a plan that never penciled.

The one-and-done borrower

The borrower who lost money on their first flip doesn't come back. They blame the deal, the market, sometimes the loan. Usually it was the analysis that was broken from day one, and nobody helped them fix it.

Rate is not a moat

Every HML in your market can match your rate this week. Racing to the bottom on points isn't a strategy. Giving borrowers a real tool with your logo on it is the kind of edge that builds loyalty and referrals.

Your logo. Your brand. Your borrowers. Powered by our engine.

License the iDeal Flip Analyzer, put your name on it, and hand your borrowers the tool that makes their submissions worth underwriting. Not a lead magnet. A working analysis platform.

The pitch rate can't match

Your competitor says "we close fast." You say "we close fast, and every borrower gets our deal analyzer so the numbers hold up before submission." That gap doesn't close on price.

Underwriting friction, down

Borrowers show up with a real ARV, a real repair scope, and real comps already run, because the analyzer forced them to. Your team spends its hours on deals that can actually fund.

Borrowers who come back

A borrower whose first flip actually penciled (didn't overpay, didn't underestimate rehab, didn't miss holding costs) is a borrower calling you for the second loan. And the third.

What your borrowers actually do inside it.

Four steps. The output is an underwriting-ready package with your logo on it. That's what lands in your inbox.

Open your branded portal

A URL on your subdomain. Every screen, every report, every login carries your brand.

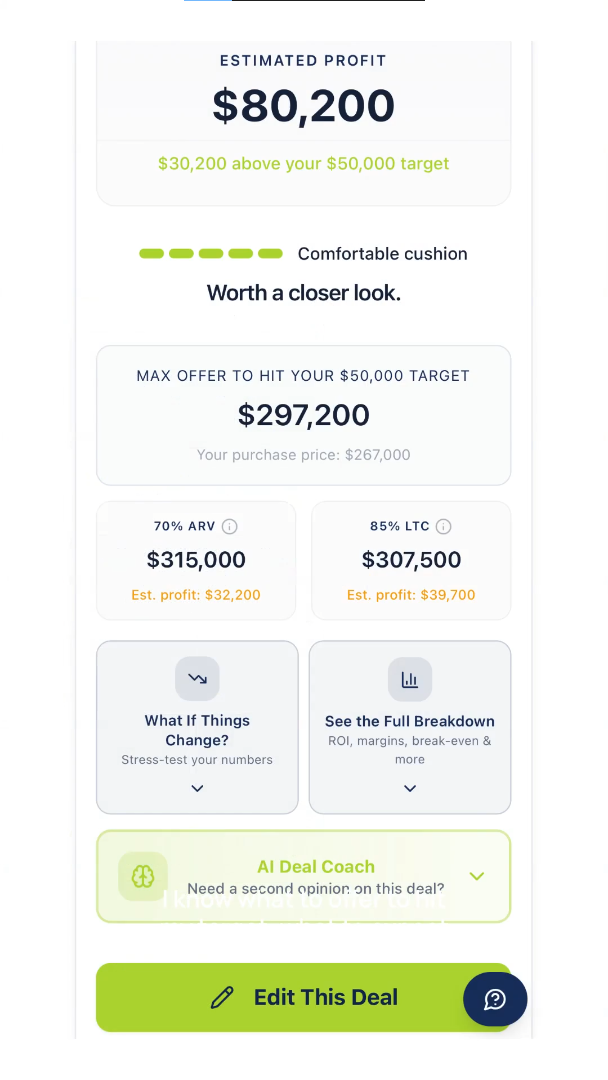

BorrowerRun the deal live

Purchase price, ARV, rehab, profit target. The AI flags soft numbers, missing costs, and comps that don't hold up.

BorrowerGenerate the report

ARV, repair estimate, profit projection, cash-to-close. A structured PDF with your logo and disclaimers.

BorrowerYou get a cleaner package

The loan file arrives with the analysis attached. The questions you'd normally chase are already answered.

LenderAn underwriting-ready package. With your brand on it.

Watch a real deal run through it.

Every deal a borrower runs generates this document, with your letterhead at the top and your disclaimers at the bottom. It reads like something your fund committee would ask for, because it was designed by someone who has sat in front of one.

- ARV backed by comps, not the borrower's optimism

- Full rehab scope by line item, AI-checked against disclosures

- Holding, selling, and cash-to-close called out plainly

- MAO with the logic shown, so pushback is a short conversation

- AI-flagged risks and things to negotiate

Everything you need. Nothing you don't.

Full white-label. Concrete deliverables. Live in about 10 business days from contract signing.

Your borrowers are already running numbers before they call you. The question is whose tool they're using.

Make it yours. Branded, accurate, and built to hand your team a file worth underwriting.

Built by someone who has sat at your desk.

Jennifer Fortier

Broker · Appraiser · Active Investor · Founder, iDeal Collective

Jennifer has spent 20+ years across mortgage origination, appraisal, title, and brokerage, through every market cycle since the early 2000s. She also flips houses in her own market, and has lost real money on bad deals (and made it back on disciplined ones).

The Flip Analyzer wasn't built by a software company selling into lending. It was built by someone who spent two decades watching borrowers submit deals that didn't pencil, and knew exactly what would fix it.

- 20+ years in mortgage origination

- Licensed appraiser background

- Title and brokerage experience

- Active flip portfolio, own capital

Flat monthly. Priced to your volume.

Every shop is different, so the exact number comes from a 15-minute conversation. The structure never changes.

White-Label License

No per-loan fees.

Your exact number depends on borrower seats, report customization, and integration work. You'll have your custom quote by the end of the demo call.

Included at Every Tier

- Full brand white-label (logo, colors, domain)

- Custom underwriting report output

- Lender backend dashboard

- Setup, onboarding, and direct support

- Founding partner rate locked for 12 months

The questions every lender asks.

Do we need dev resources or IT lift on our side?

Can we customize the report output for our lending criteria?

What happens if we cancel?

Is this a loan product, or just software?

Who owns the borrower data?

What if a borrower's flip still loses money?

Can we see a sample report before the call?

How long does the demo take?

Fifteen minutes. Straight answers.

Tell us who you are and what your loan volume looks like. We'll show you the workflow and give you your custom quote on the call.

Book a 15-Min Demo

The lenders your borrowers stay with are the ones who give them tools the shop down the street doesn't have.

If you've read this far, the question isn't whether the tool is useful. It's whether it fits your volume and your borrower profile. That's what the call is for.

Book a 15-Min Demo